Understanding scholarships and financial aid (I)

College is becoming increasingly expensive

Ever since Vanderbilt University’s total cost of attendance exceeded $100,000 two years ago, other universities such as Penn, Columbia, and USC have also seen certain programs cross the $100,000 mark.

As a result, seeking financial aid and scholarships is no longer just a concern for working-class families. Even middle- to upper-middle-income families can feel financial pressure, especially if they have two or more children attending college at the same time. Paying for college has become a real challenge for many households.

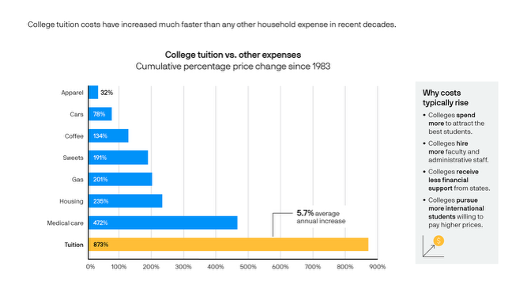

In addition, tuition has been rising at a very rapid pace. From 1983 to 2023, college tuition increased by nearly 900%, averaging about 5.7% per year. This rate is higher than inflation in housing, food, transportation, and even healthcare.

Need-aware vs. Need-blind colleges

Need-blind colleges do not consider a student’s financial situation when making admission decisions. In other words, whether a student can afford tuition does not affect their chances of being admitted. Need-aware colleges, on the other hand, do consider a family’s ability to pay when reviewing applications.

At first glance, need-blind sounds much better. But like many things, there are pros and cons. Many need-blind schools cannot fully meet every student’s financial need. For example, a student might need $50,000 in aid to afford the school, but because the available aid is spread among many students, the student might only receive $5,000. Compared to a $50,000 gap, that amount doesn’t help very much.

Need-aware schools may have a higher bar for admission, but they are sometimes able to fully meet the financial need of the students they admit. In other words, they can cover the entire gap between what a family can pay and the total cost of attendance.

You could think of it this way: need-blind spreads the aid more broadly, while need-aware targets the aid more precisely. Some people feel that need-blind is fairer to everyone, while others believe need-aware does a better job helping the students who need the most support.

Another important point is that some schools treat domestic and international students differently. For example, a university might be need-blind and meet 100% of demonstrated need for U.S. citizens and permanent residents, but be need-aware for international students. NYU is one example of a school that has this kind of policy.

Need-based v.s. Non-need-based financial aid

Need-based aid requires families to demonstrate financial need. To prove this, families must complete FAFSA or CSS Profile, and submit documents like tax returns and W-2 forms. These documents show that the family’s income is eligible for financial aid.

Need-based funding come from several sources, including federal grants, state grants, institutional grants from the college, work-study programs, and student loans.

Non-need-based aid (often called merit-based scholarships) is awarded based on a student’s academic performance, activities, or achievements. These can come from the college itself or from third-party organizations.

Usually need-based financial is much larger than merit-based financial aid. Most universities prioritize need-based aid to make sure students won’t miss college due to financial hardship. Ivy League schools and most top 20 universities typically meet 100% of demonstrated financial need, but they do not offer merit-based scholarships.

Each school sets its own income thresholds. For example, Yale considers families income below $200,000 per year eligible for need-based financial aid, and UVA’s threshold is $150,000 per year.

How much need-based aid can private universities cover?

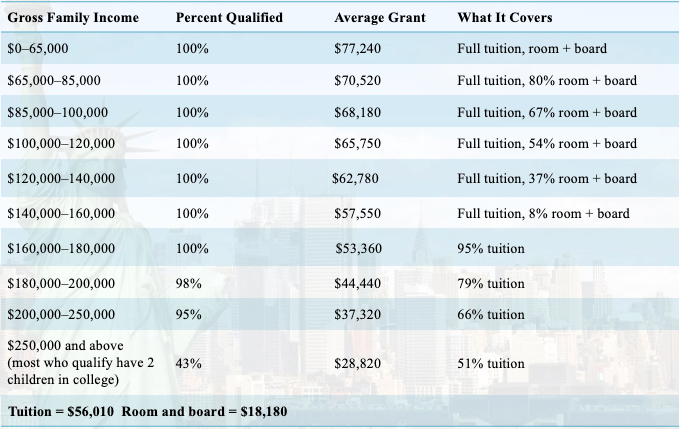

We can look at data from Princeton as an example. In theory, need-based aid does not have a strict upper limit. That means even families with incomes above $400,000 may still receive some financial aid if their financial situation is structured in certain ways.

From Princeton’s data, you can see that around $250,000 in annual family income is an important threshold. However, even for families earning above $250,000, about 43% still qualify for need-based aid, with an average award of about $28,000 per year.

FAFSA

FAFSA stands for Free Application for Federal Student Aid. As the name suggests, this is financial aid funded by the U.S. federal government.

FAFSA funding includes several types of aid. First are federal grants, which do not need to be repaid.

Second are scholarships, which may have certain requirements such as academic performance or intended major. Third is work-study. Students can earn money by working at approved jobs, either on campus or sometimes off campus.The fourth type is federal student loans, which usually have lower interest rates.

FAFSA application process

The federal deadline for FAFSA is June 30, but each college may have its own financial aid deadline. Families should always check the financial aid page on each college’s website.

The process starts with creating an account and filling out the form at studentaid.gov. Since deadlines vary by school, my advice is to submit the FAFSA as early as possible. Submitting early allows you to receive your financial aid information sooner. When college admission results come out, you can compare the financial aid packages and make a more informed decision.

After the FAFSA is submitted, the system automatically generates a report and calculates the Student Aid Index (SAI). FAFSA then sends this report to the colleges the student listed on the application. A student can send the report to up to 20 schools.

Who can submit FAFSA?

Eligibility depends on the student’s status, not the parents’ status. Students who are U.S. citizens, U.S. permanent residents (green card holders), or certain I-94 holders may qualify to submit FAFSA.

FAFSA also determines which parent is considered a contributor. This depends on several factors:

First is dependency status. The key question is whether the student is classified as a dependent on the FAFSA. Second is for married parents. If parents are married and file taxes jointly, usually only one parent needs to be listed as the contributor. Third is for divorced parents. In most cases, the parent who provided more financial support during the previous year is considered the contributor.

Families will need tax returns from two years prior. For example, students applying for college entry in 2026 will need to submit tax information starting from the 2024 tax year.

CSS Profile

CSS Profile stands for College Scholarship Service. It is a financial aid program run by the College Board. Compared to FAFSA, the CSS Profile is used by fewer schools: about 400 colleges participate.

International students may also be able to apply. However, the policies vary by school. For families that have significant financial need, I suggest focusing on colleges that participate in both FAFSA and CSS.

The CSS Profile usually opens on October 1 each year, and the deadline varies by school. Families need to check each college’s website for the exact deadline. The application is completed at cssprofile.org. You will need to prepare documents such as parents’ tax returns. Like FAFSA, the CSS Profile requires tax information from two years prior. For example, students entering college in 2026 will need to submit tax information starting from the 2024 tax year.

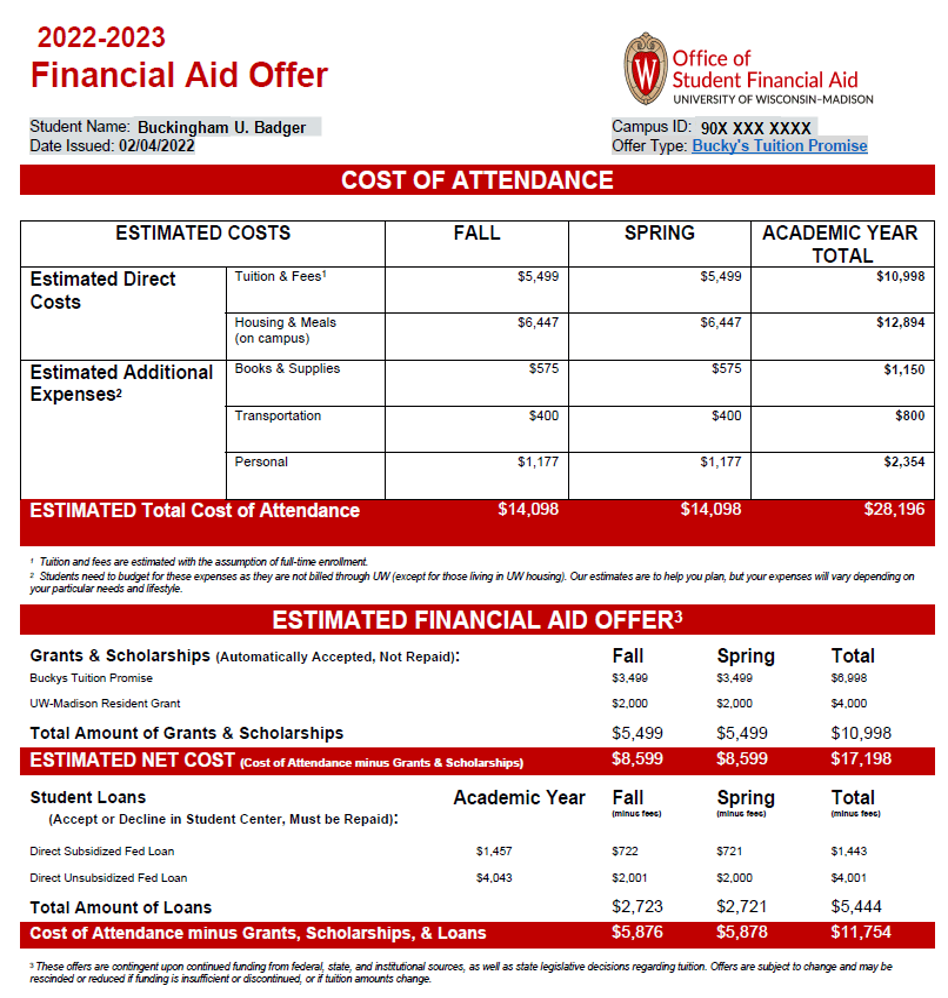

Understanding the award letter

A few months after you submit your applications, schools will send something called an award letter. This letter explains what kind of financial aid you received and how much. Once you receive it, you should review the package carefully and compare the offers from different schools.

Let’s look at an example from the University of Wisconsin–Madison. The award letter shows the estimated cost per semester and the total cost for the academic year. Then it lists the financial aid the student received. In this case, the package includes grants and low-interest student loans. After subtracting the aid from the total cost, the remaining amount is what the student needs to pay. In this example, it comes out to a little over $5,000 per semester.

One thing I want to emphasize is that when reading the award letter, you need to understand your real cost. Some people assume the school has already calculated everything. But if you look closely, there is a section called “estimated additional expenses.” These are just estimates from the school. Tuition is fixed, but other costs can vary depending on the student, things like food, housing, and transportation. So instead of relying only on the school’s numbers, families should also estimate their own realistic expenses.

How to choose between offers

When comparing offers, it helps to follow this order: First choose money you do not need to repay (scholarships and grants). Second consider money you can earn (work-study). Last consider money you need to borrow (loans).

If you are not satisfied with the financial aid package, you can submit an appeal. The award letter will usually explain how to accept the offer. In most cases, the process is simple: log into the student portal and confirm that you accept the financial aid package.

How financial aid is distributed

When the school year begins, the financial aid will be applied to the student’s account. The school will first use the funds to pay required charges such as tuition and housing. If there is any remaining amount, it will be deposited into the student’s account for other expenses.

Finally, FAFSA must be renewed every year. To continue receiving aid, it’s important to meet the requirements. First, file taxes properly and keep your tax records. Second, maintain the academic standards required by the school and remain in good standing.